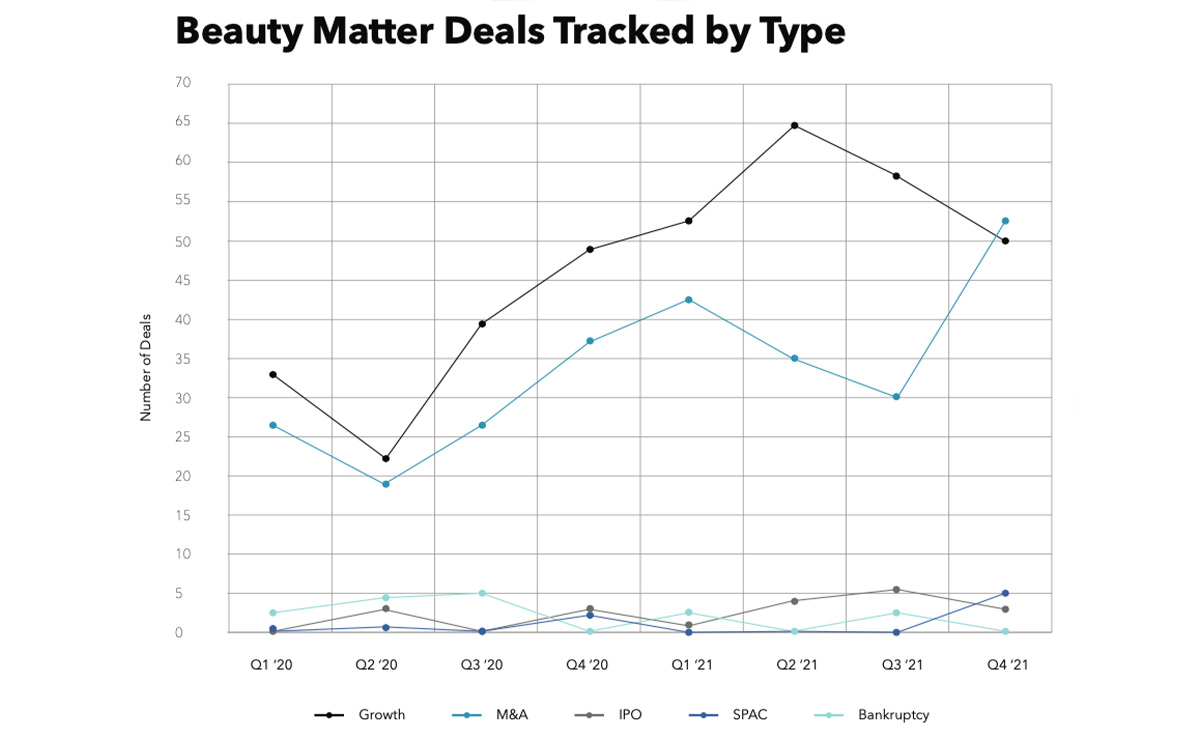

2021 was a blockbuster year for beauty and wellness dealmaking. The BeautyMatter Deal Index tracked a total of 407 deals in 2021, a 52% increase from 2020 and a 48% increase from 2019. Growth investments (seed, venture, minority stakes) dominated the deal landscape, comprising 56% of deals and growing 59% from 2020. M&A (traditional mergers, acquisitions, and majority stakes) was a close second, comprising 40% of deals and growing 46% from 2020.

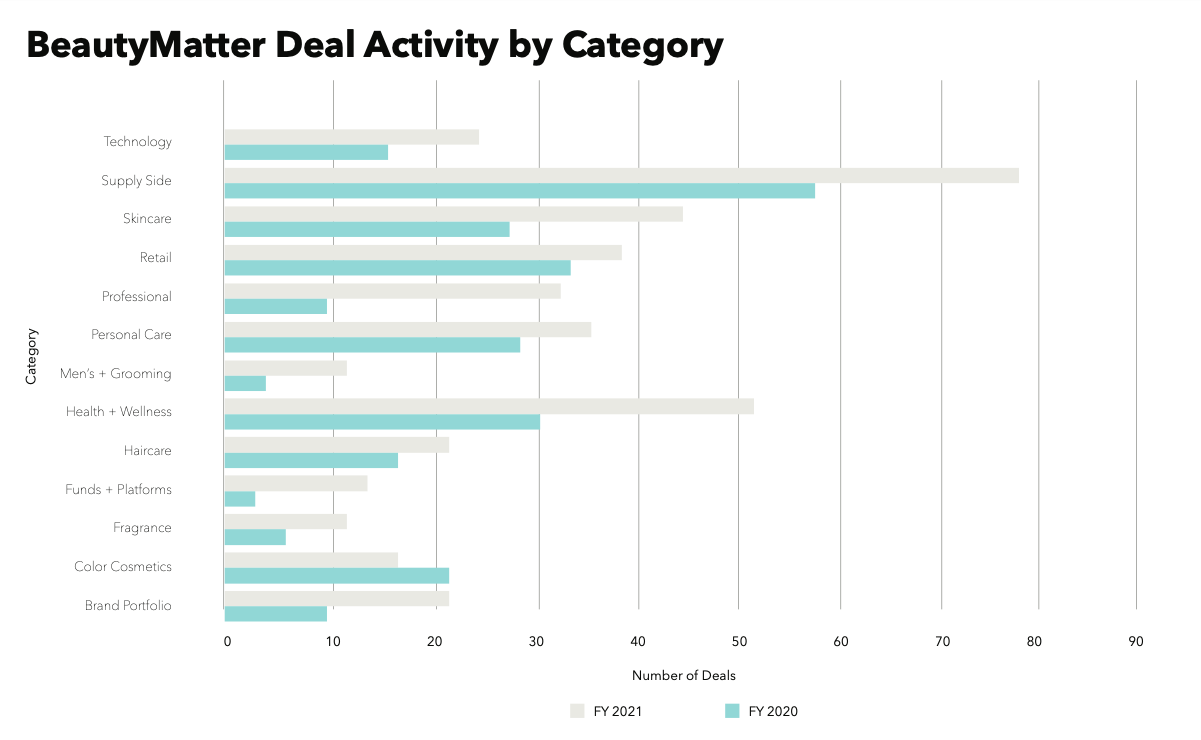

Deal momentum was strong in almost every category tracked by the BeautyMatter Deal index, with notable strength on the supply side, skincare, professional, men’s + grooming, and health + wellness. The only category to show a decline in 2021 was color cosmetics, reflecting the continued uncertainty with the category’s performance and growth given the lingering overhang from COVID and work-from-home trends.

The tremendous growth in deal activity was coupled with a continuing rise in asset valuations, with deals like Paula’s Choice trading hands to Unilever in June at a rumored 6.7x revenue multiple and Glossier raising an $80 million Series E round at a reported $1.8 billion valuation (up from $1.2 billion in 2019), despite reportedly elusive earnings. The main driver of all this activity is what we’re calling the FOMO rally—the proliferation of both strategic and financial investors looking to beauty and wellness to drive returns and growth. In the case of strategic acquirers like Unilever, Edgewell, and Procter & Gamble, it was all about competing for best-in-class brands to round out their portfolios, drive growth, tap into new consumers, and expand expertise in areas like DTC and Gen Z marketing strategies. For financial investors, it was all about finding the next generation of brands to replicate the success of previous investor exits like Advent’s September IPO of Olaplex, which was valued at $15 billion after its debut (it was $13.4 billion at the time this was written). A flurry of investors new to the beauty and wellness space has driven competition for assets and deals and, subsequently, driven up valuations. As previously reported in BeautyMatter, category interest has spurred an increase in the early-stage investment market, with investors looking at smaller deals and starting funds to place bets on the next breakthrough beauty brands. Tech-focused VCs have started investing in early-stage beauty opportunities and private equity funds have launched seed and venture funds to address gaps in the market. Greylock Partners, one of the most prominent VC firms in Silicon Valley, recently announced it would dedicate $500 million to seed rounds, making it the largest pool for early-stage start-ups ever.

To say that beauty and wellness is experiencing a bubble is a given; the real question is, how sustainable will it be? Beauty and wellness has shown astounding resilience throughout the initial COVID crisis and through subsequent shocks like the delta surge in the summer of 2021 and Omicron at year-end. With the world slowly but surely moving in the direction of opening back up, there’s a strong argument to be made that some of the fervor we saw in 2021 could extend into overlooked categories like color cosmetics in 2022. In November, we got a preview of this with Waldencast’s SPAC acquisition of Milk Makeup, and Swiftarc’s July investment in Alleyoop out of their inaugural $10 million beauty fund focused on backing disruptive innovation in female-led beauty and wellness brands. Couple this with $1.9 trillion of dry powder burning a hole in investors’ pockets, and all signs point to continued deal activity as we head into 2022.

Economic Trends Investors Will Be Focused On in 2022

Inflation: In December, the US Labor Department reported that inflation, as measured by the consumer price index (CPI), had risen by 7%, the fastest 12-month pace in nearly 40 years. The move comes amid a shortage of goods and workers in an economy flush with cash from government COVID stimulus and moves by the Federal Reserve to prop up the economy over the last two years. This means that consumer wallets are feeling pressure as everything from food to energy costs get more expensive. This could have a material impact on beauty and wellness if consumers redirect discretionary spending away from beauty and into essentials. Early data is showing that this has not been the case, however, as consumers continue to shop and some analysts are predicting the spending boom of 2021 will extend into 2022. According to the National Retail Federation, retail sales during 2021’s November-December holiday season grew 14.1% over 2020 to $886.7 billion, easily beating their forecast and setting a new record despite challenges from inflation, supply chain disruptions, and the ongoing pandemic.

Rising Interest Rates: Federal Reserve officials announced in mid-December that they are prepared to fight inflation with as many as three rate hikes, starting this spring. This could have an impact on larger deals that rely on leverage for funding as borrowing costs would increase. Rising rates could also have an impact on deals reliant on the public markets like SPACs and IPOs as interest rate increases have the potential to create volatility in the stock market.

Worker Shortages: As we begin 2022, jobs are plentiful but workers are not. As a result, labor costs have increased as companies compete for workers that are in short supply and do even more to retain their best workers. Shortages and phenomena like the “Great Resignation” have had a particularly poignant impact on small and mid-sized businesses but, ultimately, every business is impacted by this as worker shortages contribute to supply chain issues and reductions in services. Worker shortages are expected to persist throughout the year but, according to a survey by KPMG, one-third of executives surveyed want to use M&A to acquire talent in 2022, so, it could help fuel deal activity among targets with exceptional teams.

Supply Chain Issues: By now everyone has heard about the supply chain issues that resulted in shortages and price increases throughout 2021. Unfortunately, most experts agree that these issues are here to stay through most of 2022. This has manifested itself in beauty and wellness, with brands being sold out of best-sellers for months because they can’t get components, manufacturers short on key ingredients so they can’t ship product, and retailers unable to replenish because of product shortages. This has resulted in both top-line and bottom-line pressures for businesses, has been a major contributor to inflationary pressures, and has been exacerbated by worker shortages.

US-China Relations: No discussion of the beauty and wellness supply chain would be complete without mentioning China and the impact any disruption of US-China relations could have on the industry. Most brands and retailers are heavily reliant on China for everything from packaging components to ingredients to shipping materials to the PPE they provide their employees at work. Then, of course, there’s the tremendous growth opportunity for US brands looking to capture the attention of consumers in the world’s number-two beauty market. Recent tensions with Beijing over issues like Taiwan, the treatment of the Uyghur population in the Xinjiang region, and changes in Hong Kong have the potential to come to a head in 2022 and create friction for the trading relationship between the two superpowers.

SPAC Regulation: In early December, SEC Chair Gary Gensler announced that he’d like to see tougher regulation of SPACs (special purpose acquisition corporations). Specifically, he mentioned new rules around marketing practices, tougher disclosure requirements, and liability obligations for SPAC “gatekeepers,” which could include sponsors, financial advisors, and other bookkeepers. SPACs have been a popular investment vehicle for beauty and wellness, with the BeautyMatter Deal Index recording six deals in 2021, five of them in the fourth quarter. New regulations could make the investment vehicle a less attractive option as investors structure deals in the space.

Midterm Elections: In November, the US will hold midterm elections, which has the potential to change control of Congress and the Senate. The outcome of the elections could impact policies around taxes, regulations, domestic spending, and foreign trade, all of which could impact dealmaking in the latter part of the year and going into 2023.